Scenarios for the coming months: banking crisis, recession, crash?

W. 1 Selected stock indices from March 08.03.2023, XNUMX. Source: own study, stooq.pl

From March 8. the difference between the Nasdaq100 and the WIG20 is as much as 14,8 percentage points (and this is only slightly over 2 weeks). It is no better since the beginning of the year, where the difference is 23,5 percentage points. Details of the rates of return in different periods for the above indices are presented in the table below. What is interesting in the table below is the fact that Nasdaq100 "wins" with WIG20 in every period except 2022.

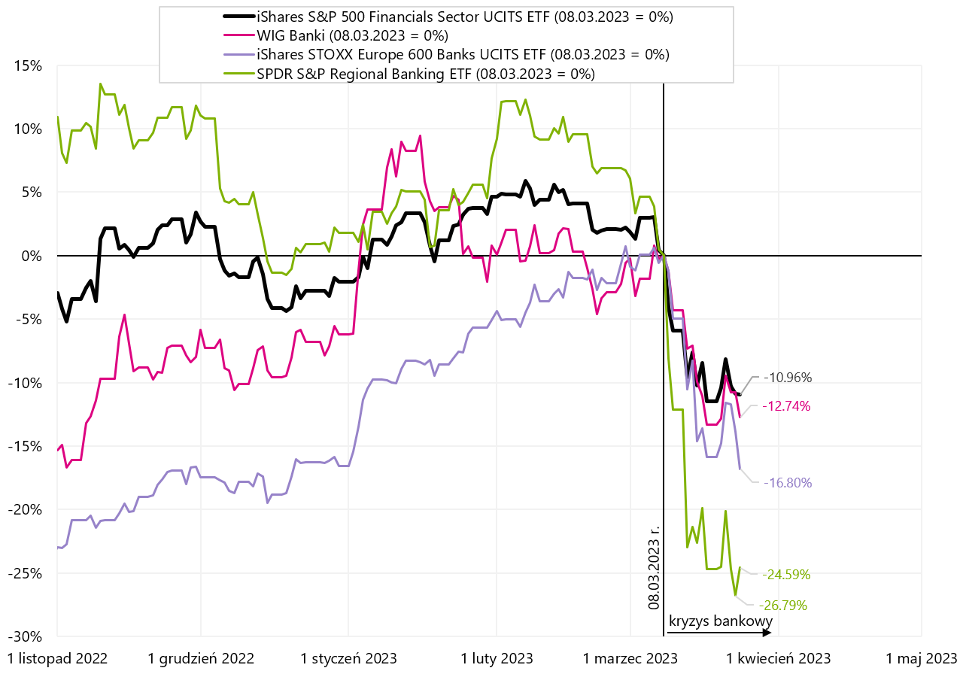

W. 2 Selected banking indices from March 08.03.2023, XNUMX. Source: own study, stooq.pl, ishares.com

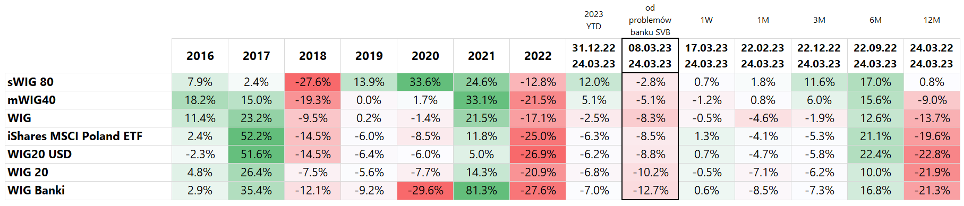

W. 3 Polish indices from March 08.03.2023, XNUMX. Source: own study, stooq.pl

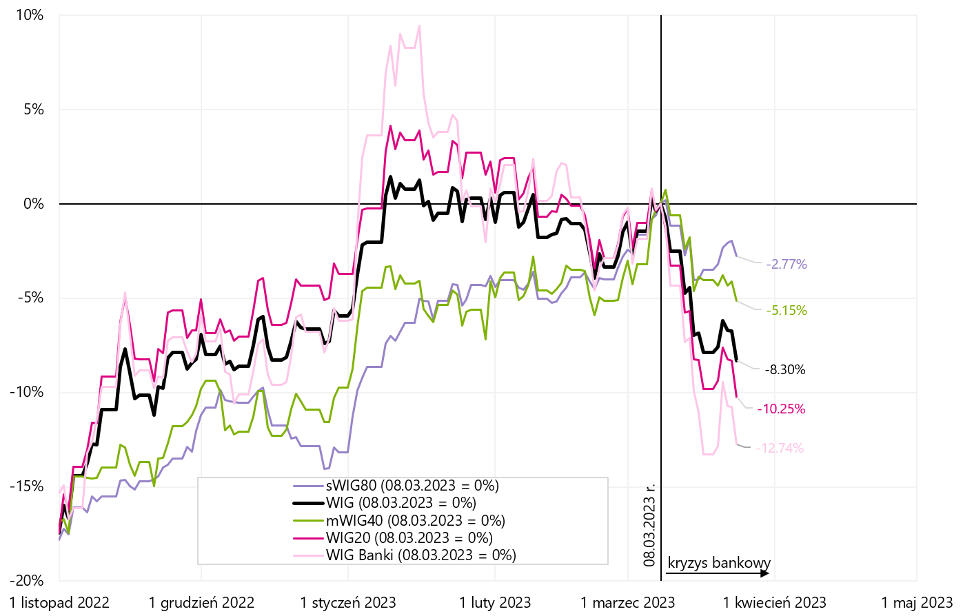

W. 4 American, European and Polish treasury bonds from March 08.03.2023, XNUMX. Source: own study, ishares.com, stooq.pl

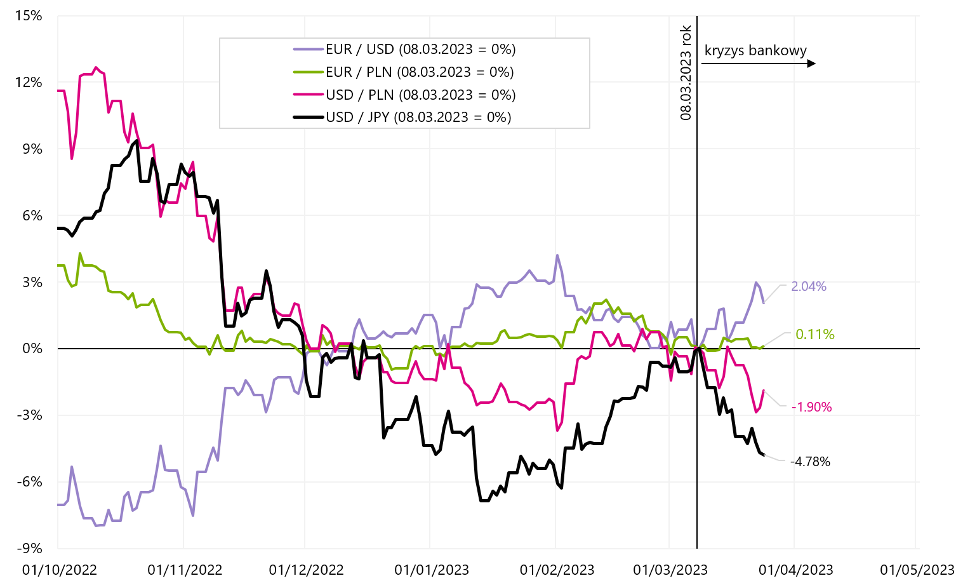

W. 5 Rates of selected currency pairs from March 08.03.2023, XNUMX. Source: own study, stooq.pl

About the Author

Jaroslaw Jamka - Experienced fund management expert, professionally associated with the capital market for over 25 years. He holds a PhD in economics, a license of an investment advisor and a securities broker. He personally managed equity, bond, mutli-asset and global macro cross-asset funds. For many years, he managed the largest Polish pension fund with assets over PLN 30 billion. As an investment director, he managed the work of many management teams. He gained experience as: Member of the Management Board of ING PTE, Vice-President and President of the Management Board of ING TUnŻ, Vice-President of the Management Board of Money Makers SA, Vice-President of the Management Board of Ipopema TFI, Vice-President of the Management Board of Quercus TFI, Member of the Management Board of Skarbiec TFI, as well as Member of Supervisory Boards of ING PTE and AXA PTE. For 12 years he has specialized in managing global macro cross-asset classes.

Jaroslaw Jamka - Experienced fund management expert, professionally associated with the capital market for over 25 years. He holds a PhD in economics, a license of an investment advisor and a securities broker. He personally managed equity, bond, mutli-asset and global macro cross-asset funds. For many years, he managed the largest Polish pension fund with assets over PLN 30 billion. As an investment director, he managed the work of many management teams. He gained experience as: Member of the Management Board of ING PTE, Vice-President and President of the Management Board of ING TUnŻ, Vice-President of the Management Board of Money Makers SA, Vice-President of the Management Board of Ipopema TFI, Vice-President of the Management Board of Quercus TFI, Member of the Management Board of Skarbiec TFI, as well as Member of Supervisory Boards of ING PTE and AXA PTE. For 12 years he has specialized in managing global macro cross-asset classes.

Disclaimer

This document is only informative material for use by the recipient. It should not be understood as an advisory material or as a basis for making investment decisions. Nor should it be understood as an investment recommendation. All opinions and forecasts presented in this study are only the expression of the author's opinion on the date of publication and are subject to change without notice. The author is not responsible for any investment decisions made on the basis of this study. Historical investment results do not guarantee that similar results will be achieved in the future.