are recording the largest daily outflow of funds in history")

Ahead of the ECB meeting: hold the fort at all costs

The downward revision of the ECB experts' projection will increase expectations of future aggressive interest rate increases. The ECB will probably consider the situation on the labor market as a reason to keep rates high for longer. The importance of US monetary policy for the ECB will increase as the euro risks sharp devaluation if the ECB softens its stance too early. The market will be on the lookout for any mention of the Pandemic Emergency Purchase Program (PEPP).

Due to the fact that the valuation of bond futures contracts include five interest rate cuts in 2024. starting in March, the ECB has ample room to maneuver to lower such expectations in the face of looser financial conditions and stable sovereign bond spreads in the coming weeks.

Germany and the Netherlands in recession

The meeting will be in the spotlight this week European Central Bank on monetary policy, as well as the FOMC and Bank of England meetings.

Bond futures valuations take into account a 50% probability that the ECB will start cutting interest rates in March next year, making a total of five rate cuts in 2024. This means that the ECB is expected to start cutting interest rates earlier than the Fed and the Bank England. This opinion is confirmed by inflation data for the next three months, which surprised negatively, falling to 2,4% y/y - the lowest level in over two years. Moreover, the economy in the euro zone slowed down significantly, with Germany and the Netherlands falling into recession.

For several weeks, information has been circulating that a number of ECB representatives are slightly softening their stance, emphasizing the need to reduce interest rates next year to avoid further economic damage. The latest such case concerns a well-known "hawk": Isabel Schnabel, who until last month maintained that rate increases should still be an option. In her last speech, Schnabel stated that further rate increases are unlikely and allowed for the possibility of rate cuts in mid-2024.

ECB experts' projections in the spotlight

Although Lagarde will maintain his aggressive stance, updates to the ECB experts' projections may prove to be a more important signal. In September, these projections predicted a decline inflation base rate to 3,2% this year and to 2,1% in 2024, while real GDP was expected to end 2023 at 0,7% and 2024 at 1%. Since both GDP and inflation have been surprising negatively so far, we can safely assume a downward revision of both data both this year and next. The lower the projections, the more markets will expect aggressive cuts in interest rates.

The ECB still has reasons to continue its aggressive policy

The situation on the labor market will remain a problem for the ECB in the context of inflationary pressure in the euro area. Unemployment remains at 6,5% - the lowest in history. Even though wage pressure is starting to ease, it remains above 5% (of wages per employee), which is too high to ensure a return to the ECB's 2% inflation target. Therefore, the central bank may not be in a hurry to return to dovish rhetoric this week, instead holding off on a decision for an extended period of time, putting into doubt next year's rate cuts currently factored into market valuations.

It should also be remembered that whatever happens in the United States will also have an impact on future decisions regarding monetary policy on the Old Continent. An even stronger labor market in the United States suggests that aggressive rate cuts by the Fed in the near term are unlikely. If expectations for US rate cuts are postponed until 2025, we can expect rate cuts to be postponed in Europe as well. If the ECB cuts rates too early, it risks a sharp devaluation of the euro, which could increase inflation.

Therefore, Lagarde will rather seek to counteract earlier rate cuts than to soften its stance. Reinvestments under PEPP (Pandemic Emergency Purchase Portfolio), which were to remain unchanged until the end of 2024, can be used as an argument in the fight against expectations regarding the upcoming cycle of cuts. A few weeks ago, Lagarde mentioned that PEPP will have to be re-examined in the “not too distant future.”

PEPP will be in the spotlight

PEPP has proven to be a valuable tool for the central bank because it allows it to target its bond purchases towards government bonds of those countries where spreads treasury bonds relative to German bonds, they are expanding excessively. Therefore, if PEPP is discussed at the next meeting, it will not only make it possible to set the earliest possible date for anticipatory interest rate cuts, but may also deal a blow to the so-called peripheral countries.

Let us assume that the policy of ending reinvestment under PEPP will be implemented already in January 2024. In such a case, it would be unlikely that at the next monetary policy meeting in March a decision would be made to make a pre-emptive cut. This should be enough for markets to postpone the likelihood of the first rate cut until April or June.

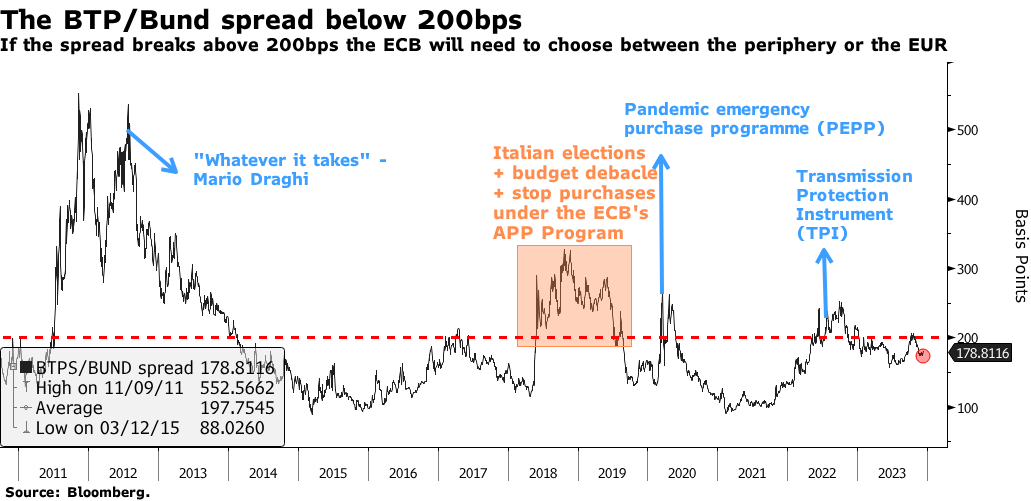

However, we believe that it remains a key indicator of the ECB's monetary policy yield spread of Italian and German government bonds. It has narrowed significantly over the past few months, falling to 180 basis points from 206 basis points in October. Combined with the fact that, according to the Bloomberg Economics index of financial conditions in the euro zone, economic conditions have relaxed to the levels seen before the summer, the ECB is unlikely to feel the need to cut rates anytime soon. First of all, it will focus on how to maintain an aggressive policy without market expectations of rate cuts, as was the case in November.

If the spread of Italian and German government bonds widened above 200 bp and headed towards 250 bp, it would be a sign that the central bank is starting to feel uncomfortable with its restrictive policy and that monetary policy easing could be expected.

About the Author

Althea Spinozzi, Marketing Manager, Saxo Bank. She joined the group Saxo Bank in 2017. Althea conducts research on fixed income instruments and works directly with clients to help them select and trade bonds. Due to his expertise in leveraged debt, he focuses particularly on high yield and corporate bonds with an attractive risk-to-return ratio.