A thaw at the Fed is needed to ensure a lasting return on the USD exchange rate

Unless in the coming quarter there is a sudden resumption of Russian natural gas flows to Europe, for Europe and the euro, as well as satellite currencies - the pound sterling and the Swedish krona - economic winter is coming. Although the ECB and other central banks - with an extremely significant exception Bank of Japan - caught up with the Fed in terms of tightening policy in the third quarter, Federal Reserve it remains the central bank that "rules everyone". The Fed will have to ease its policy again before we can be sure that the US dollar is finally ready to reverse.

USD: Fed returns to its old rhetoric after trying to slow down policy

The US dollar peaked temporarily in the wake of a press conference FOMC on June 16, when the market decided that the first 1994% interest rate hike since 0,75 will turn out to be the peak of the Fed's hawkish policy in the current cycle. On the day following the FOMC meeting, the bear market in the stock market reached the minimum level of the cycle, not exceeded as at the date of writing this text. Risk sentiment found further fuel, and ahead of the FOMC meeting in late July, the dollar slumped slightly as Powell failed to provide enough support to the market, which began pricing in that the Fed's interest rate would peak as early as December 2022 and begin to decline as early as December 2023. in the first half of 100 However, from the beginning of August, Fed members quickly began to explicitly refute the accusations of forecasting any Fed policy easing, presenting almost 8% consistently aggressive rhetoric. The dollar appreciated again, even though many other central banks were even more aggressive in raising rates and guidelines. At the meeting on September XNUMX EBC it even raised the interest rate by 75 basis points, which was the largest hike in the history of this central bank.

About the Author

John Hardy director of currency markets strategy, Saxo Bank. Joined the group Saxo Bank in 2002 It focuses on providing strategies and analyzes on the currency market in line with macroeconomic fundamentals and technical changes. Hardy won several awards for his work and was recognized as the most effective 12-month forecaster in 2015 among over 30 regular associates of FX Week. His currency market column is often cited and he is a regular guest and commentator on television, including CNBC and Bloomberg.

After the remarkable thaw in financial conditions since the FOMC meeting in June, despite the first 75bp "super-hike" at that meeting, the Federal Reserve apparently recognized that it would gain more by maintaining aggressive rhetoric than trying to prepare the market for an imminent political turnaround in related to some abstract concept such as the neutral rate. The Fed probably sees now that it is easier to pull back after an over-tightening crash than to risk increasing inflationary risks by relaxing financial conditions in the middle of a tightening cycle in an attempt to win over the market through the guidelines.

One factor that increased the potential for a rebound in the US economy in the fourth quarter was the sharp fall in gasoline prices after hitting a record high of $ 5 per gallon in early June. A drop well below $ 4,00 already in August could have a significant real and psychological impact on the legendary US consumer and keep the economy and wage pressures afloat slightly longer than anticipated in this cycle, requiring the Fed to hold the rate and continue attempts to achieve the full pace of quantitative tightening - as announced in September, the pace of balance sheet reduction should amount to USD 95 billion per month. Hence our economist Steen Jakobsen predicts "peak tightening" in the coming quarter.

Risk tail of risk warning for USD in QXNUMX: mid-term elections

The mid-term elections are an important risk event in the tail of the decay in Q70 for the long-term forecast of likely US policy responses in the event of the next recession or downturn. Analysts and bookmakers assure that while the Democrats are likely to consolidate their majority in the Senate, they will almost certainly lose control of the House. It may be so, but the last two election cycles have taught us to treat election polls more distantly, and in our opinion, the surprise potential has been dramatically increased by two events: the US Supreme Court, staffed by Trump-nominated judges, overturned the Roe v. Wade verdict from the 2020s, guaranteeing access to abortion at the federal level, and the victory of Democrats in a series of special elections in districts so far voting for Trump in recent months - in particular in the election for representative of the House of Representatives in Alaska, in which Trump supporter Sarah Palin lost to the Democratic candidate . Alaska is a state that voted 10 points ahead of Trump in 9 and the Republican candidate for the House of Representatives 2024 points ahead of an independent opponent in the same election. In a deeply divided political environment, the United States can only pursue fiscal policy if one party does not control both houses of Congress and does not have a president of its own. There are notable exceptions, including issues where both parties speak with one voice, such as addressing supply chain weaknesses with China and restricting Chinese access to military and advanced technologies. In any case, if the Democrats surprise everyone and retain control of the House of Representatives, coupled with stronger Senate control, this could completely reverse the scenario of fiscal policy potential ahead of the US presidential election in 2, overall increasing the risk of significantly higher inflation outcomes. . If Biden won just one or two more seats in the Senate in the last two years, his party could have passed a package of about $ XNUMX trillion larger than what was actually pushed through in the so-called the inflation act.

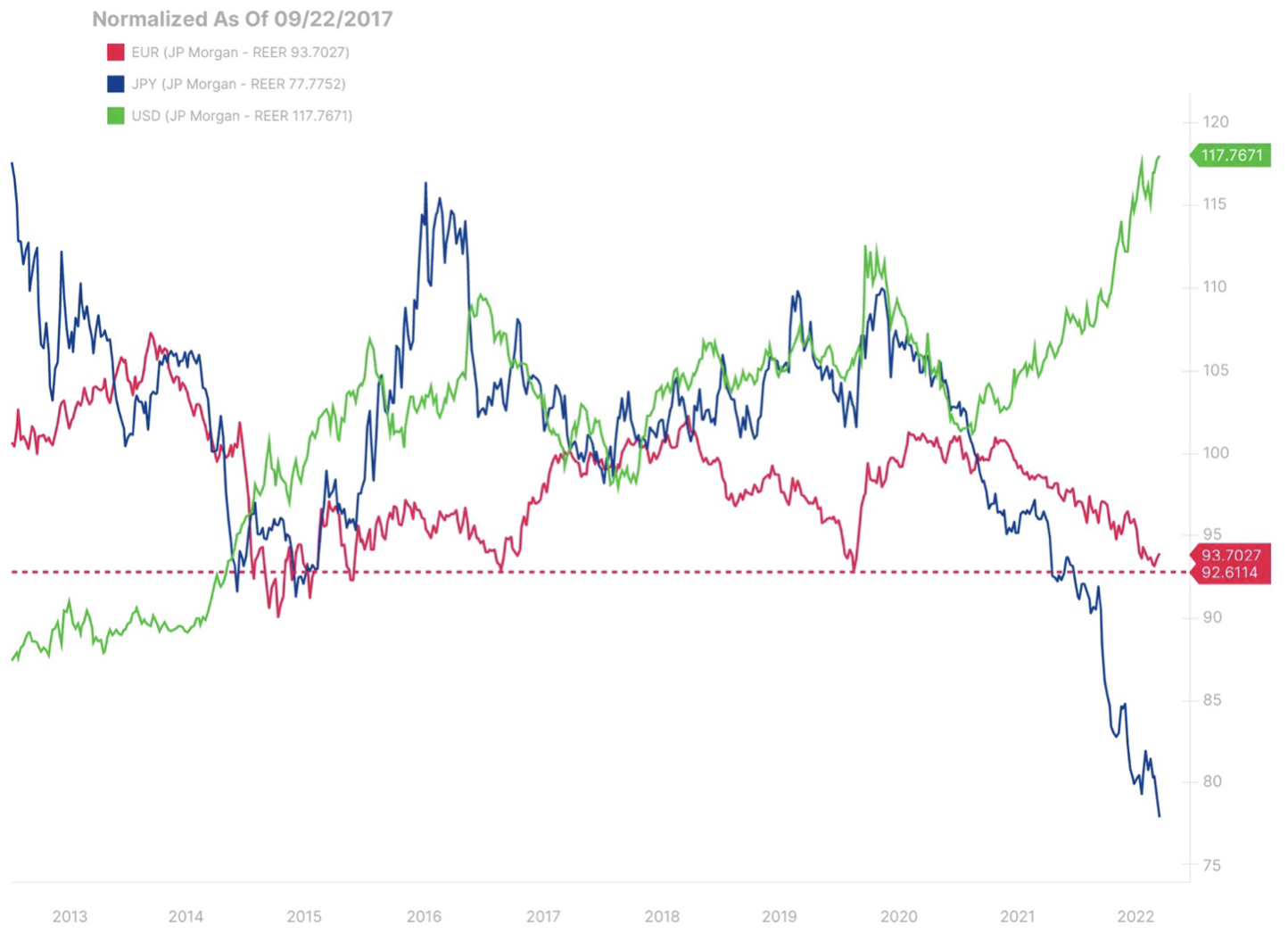

Jaws dilate dangerously! Since mid-2021, there has been a widening discrepancy in performance between the rapidly rising US dollar and the weakening euro and the even weaker yen. It should be noted that the indicators are adjusted for the CPI and the Japanese retail CPI measures have probably been relaxed, which means that the situation could be even worse. In the fourth quarter there may be a breakthrough in the efforts of the Bank of Japan to limit profitability. Let us note that the weakening of the euro seems small in comparison, even after temporarily falling below parity several times in the third quarter.

EUR, GBP and winter discontent

The euro fell below parity against the US dollar due to intense and excessive pressure on inflation in the EU from soaring energy and electricity prices, which also posed a risk to production volumes and had a truly seismic impact on the external balance sheet. From the economic bloc with the world's largest trade surplus, Europe has turned into a deficit region in the world, heading towards an economic slowdown and likely recession in QXNUMX and early next year.

Much has been said about the EU's heroic efforts to build warehouses natural gas before the heating season begins in autumn, however, they will not provide the necessary additional supply unless Russian gas flows again during the winter - unless demand in the EU drops further. If President Putin or anyone like him remains in power in Russia, the long-term picture of Europe's energy supply will remain problematic as the EU will have to continue to secure LNG supplies in a limited world market. There may be new sources of gas - perhaps in the long term from Algeria, and in the coming months - from a new entrant in the LNG market, Mozambique. However, the energy outlook for the EU is likely to never turn out to be as bad as it is for the coming winter of discontent; in the coming quarter or at the beginning of next year, the euro may therefore reach a significant minimum. The EU's price containment plans may help bring down EU nominal inflation readings in the coming months, but it will not choke demand. Physical constraints on natural gas supplies, perhaps compounded by the risk that French nuclear power plants will not be fully operational by late winter, may force energy rationing and a decline in real GDP. Europe will count on a mild winter, and daily and weekly weather forecasts will be treated with more attention than ever in the history of the continent. The same is true for the UK, and the icing on the cake is that the UK does not have strategic gas storage facilities, although it is making efforts to do so. We repeat: winter is coming and it will come every year, but the EU, on the wave of existential concerns, will quickly start resolving its problems.

Britain should be watched closely as a country capable of a more flexible and decisive political response than any other large country, given the combination of enormous pressure on the British economy from external deficits and the cost of living crisis on the one hand, and the new prime minister Liz Truss and her the mentality of "I have nothing to lose" on the other. Her instincts will be to act quickly and decisively to provide the country with light and warmth in the coming winter, but also to ensure that through political action, the UK emerges from its current plight and weakness. If Liz Truss wants to remain in the prime minister's seat for longer, the UK must find a new path towards balancing its external deficits and reducing energy sensitivity. Its approach of populist price controls on the one hand and tax cuts on the other is risky for the pound sterling due to the implications for the national deficit. The pound sterling could see further declines this winter as long as European energy prices remain decidedly high (natural gas in particular is a critical factor). In the long run, for pound sterling to rise from the ashes, politics will need to be effective in attracting investment, increasing UK domestic energy production (unlocking UK shale gas potential?) And improving productivity. To put this into perspective: the pound is not even fully incinerated anyway, because we note that in terms of CPI-adjusted real effective exchange rate it is actually only halfway between the collapse of the initiated referendum on Brexitu in 2016

Continuing tension among Asian giants CNH and JPY

In both recent forecasts, we highlighted the still very stretched CNY / JPY rate. CNH loosely follows the US dollar, while the JPY remains the weakest currency among the G10 currencies as the Bank of Japan refuses to tighten its policy and deviate from its yield curve control policy. In the third quarter, the CNY / JPY exchange rate reached new long-term highs well above 20,00. Will the fourth quarter prove to be the one in which something "breaks" here? On the CNY (and closely tied CNH trading currency) side, China may decide that it is simply no longer in their interest to keep the currency strong, especially if commodity prices begin to fluctuate due to a worsening economic outlook. However, it is more likely that the Bank of Japan will capitulate through the strengthening of the JPY, which was discussed in our forecast for QXNUMX.

Significant further downward pressure on the yen may simply force the Bank of Japan to surrender after so long holding in the hope that wage growth will prove sufficient to suggest a persistently positive inflation outlook. However, there may also be an 'egg and chicken' problem in the Bank of Japan's inflation and inflation risk measures: it concerns the policy of Japanese supermarket chains to keep food prices restrained even when wholesale and import prices have risen sharply, which has even more aggravated by cheaper JPY. An overnight reset of consumer prices is expected on October 1, which could lead to a spike in official inflation readings and a growing public anger over the rising cost of living. Fiscal attempts to shield lower-income households will not help JPY or ease the fears of middle- and higher-income people. Will QXNUMX prove to be a quarter in which the Kuroda-led central bank will surrender and change its guidelines, or at least shift the yield curve control targets? There is enormous bi-directional volatility potential for JPY pairs, particularly if the USD / JPY pair reaches aggressive new decades of highs before the Bank of Japan finally capitulates.

Other G-10 currencies

In this case, "other G-10 currencies" are Swiss Franc (CHF) and "small G-10s" including AUD, CAD, NZD, SEK and NOK. Regarding the CHF, with the maximum increase in pressure on the cost of living in the coming winter, the Swiss National Bank will be happy to continue its policy of tightening and supporting the stronger franc, which has significantly helped to contain the inflationary pressure in Switzerland. For the smaller G-10 currencies, the "tightening peak" we forecast in Q1,1300 is likely to be unfavorable for less liquid currencies. Regarding the Antipodes - AUD and NZD - we wonder if the AUD / NZD pair will be able to break through the multi-year XNUMX range in which it has held for more than seven years, given Australia's massive raw material portfolio and its new status as a country with a current account surplus, while New Zealand depends on energy imports. New Zealand also raised rates quickly and therefore is likely to be in the lead of countries where there will be a slowdown and a possible pause in rate hikes.

In Europe, Norway will have to play a part to some extent with the European movement to curb energy prices after the country has made substantial gains from soaring prices, notably natural gas. The Swedish Krona seems cheap, however it may need to go down for its outlook to improve permanently given its history as one of the more sensitive currencies to economic outlook and risk appetite.