A perfect storm in the form of a tightening of the Fed's policy and fear of recession

Markets have recently struggled with the dual problem of fear of inflation and fear of recession. Recession or not, the dynamics of the US economy in the second half of the year will slow down as accumulated demand slows down and interest rates rise. Coupled with a recession in corporate earnings, this means the downside potential for equity markets may be greater. Bonds may regain prominence as a portfolio diversification tool, but a consistent target in a bear market should be to improve portfolio 'quality'.

The demand side in focus

While the focus has been on supply constraints over the past few months, the demand side of this equation now needs attention as cumulative demand begins to slow down and central bank tightening begins to take its toll.

Markets will continue to oscillate between inflation fears and recession fears over the next few weeks as a quick fix is unlikely to be the case. Inflation is likely to remain high in both the US and the UK / euro area, while macro data will continue to deteriorate as higher interest rates begin to impact both sentiment and activity. We are more concerned about the increasing risk of policy error because Fed it tries to restore equilibrium while trying to stop the inflationary engine.

Darkness and fear

A series of mistakes in the Fed's research resulted in a more cautious approach to the US economy. However, it must be admitted that the discrepancies in survey data and their potential for misleading depend on how the questions are constructed.

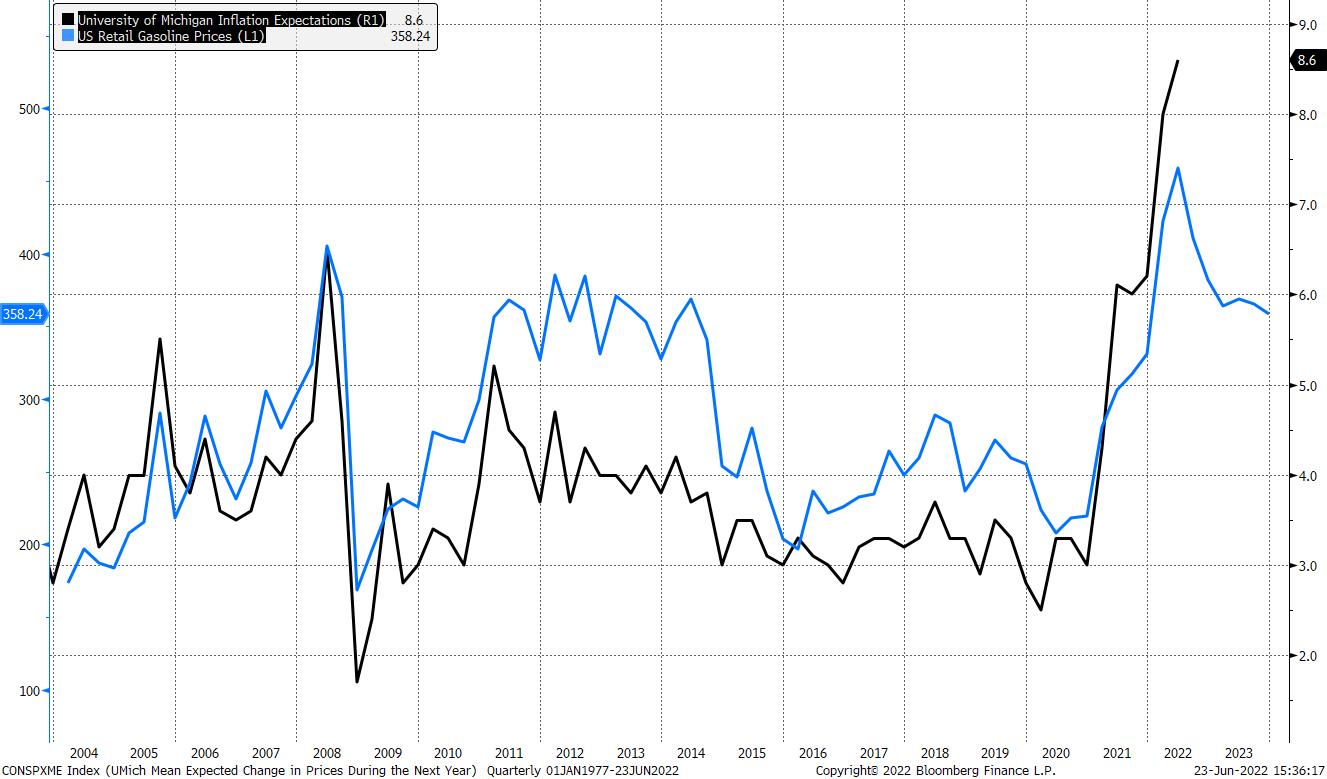

Overall survey result University of Michigan for June it fell to a record low of 50,2 compared to the previous 58,4, and both the expectations index (46,8 from 55,2) and the current conditions index (55,4 from 63,3) went down sharply . Meanwhile, according to the Conference Board, consumer confidence remains unchanged. The University of Michigan is likely to be focusing more on the inflation / cost of living dynamics that are currently hitting consumers notably due to the rise in gasoline prices. As can be seen in the chart below, inflation expectations in the University of Michigan's poll closely follow retail gasoline prices, which may be due to the way the survey's questionnaire is constructed. By contrast, the questions in the Conference Board's survey are more focused on the labor market and household incomes, which have so far not suffered much.

Even so, data on real economic activity, including retail sales, housing and manufacturing, have deteriorated significantly, suggesting there are reasons to be cautious. The decline in retail sales is a warning of the destruction of demand, while the weakening demand for houses and apartments due to higher costs of loans indicates the possibility of a real estate market crash.

Are these signs of an impending recession?

The technical recession means two consecutive quarters of negative GDP growth. Considering that US GDP in Q1,5 was -XNUMX%, and the GDPNow model adopted by the Federal Reserve Bank in Atlanta points to a flat QXNUMX, it means that the probability of a technical recession is high.

However, the National Bureau of Economic Research (NBER) defines a recession as "a significant decline in economic activity that covers the entire economy and lasts more than a few months." This applies to real personal income less transfers, employment in the non-agricultural sector, real personal consumption expenditure, price-adjusted wholesale and retail sales, employment as measured by a household survey, and industrial production.

So far, the data on these indicators are solid. Employment growth in the non-agricultural sector slowed down to 390 thousand. in May from levels exceeding 500 thousand. recorded in the months leading up to January, however, still signals strong labor demand and a broad labor market. Real incomes and expenses are rising, and favored by the Fed inflation rate core PCE rose by 6,3% YoY in April, exceeding the estimates. There is no doubt that the dynamics of the US economy will slow down, but it does not seem likely to collapse. The shift in demand from goods to services will continue to support employment, income and expenditure growth. However, pressure on the cost of living suggests that households are exhausting their savings and taking more loans to finance them. Consumer sentiment may change in the second half of the year as fears of a recession build up, suggesting a lower contribution of consumer spending to overall economic growth in the second half of the year.

Corporate earnings recession is coming

As interest rates go up, the markets generally lower equity valuations. However, as fears of a recession build up, the earnings outlook also worsens. In the first quarter, most companies expected an increase in cost pressure, and in the face of increasing supply and wage pressure, we can expect disappointing profits from mid-July. fact set estimates that in the second quarter, the growth in profits of companies from the S&P 500 index will drop to 4,3%, which will be the lowest increase since the fourth quarter of 2020 (3,8%).

Market implications

Recessions tend to have the greatest impact on cyclical actions and sectors such as energy, industry and technology equipment. While the limited supply in the energy sector may save these sectors from significant losses this time, they should be approached with great caution.

Defensive sectors such as consumer staples, utilities and the healthcare sector tend to perform better. As inflation was more important than other macroeconomic problems in the first half of the year, bonds were not the best hedge for portfolios either. Perhaps this narrative will reverse in the second half of the year as lower commodity prices help cool inflation and central banks begin to focus on economic growth. This may cause the share of fixed income products in the portfolios to increase again, with the benefits of diversification, but it will depend on whether or not inflation retreats.

The first thing to remember is that a long-term investor is most likely to make maximum portfolio gains on positions taken during the bear market. As stock markets continue to decline, dollar cost averaging appears to be the best strategy to build up those high-quality (steady cash flows, reliable earnings streams and controlled debt levels) growth stocks that will drive our portfolios over the long term.

More Saxo analyzes are available here.

Charu Chanana, market strategy, Saxo Bank