The importance of operating margin in times of inflation

Since inflation started accelerating in early 2021, industrial companies with low margins are underperforming compared to high margin companies.

The market recognizes that companies with low margins are more sensitive to persistent wage pressure. While this short-term pressure can be alleviated through cost-cutting and layoffs, long-term competition against rivals with higher margins could prove disruptive in the long run as low-margin companies lose employees and acquire fewer talent.

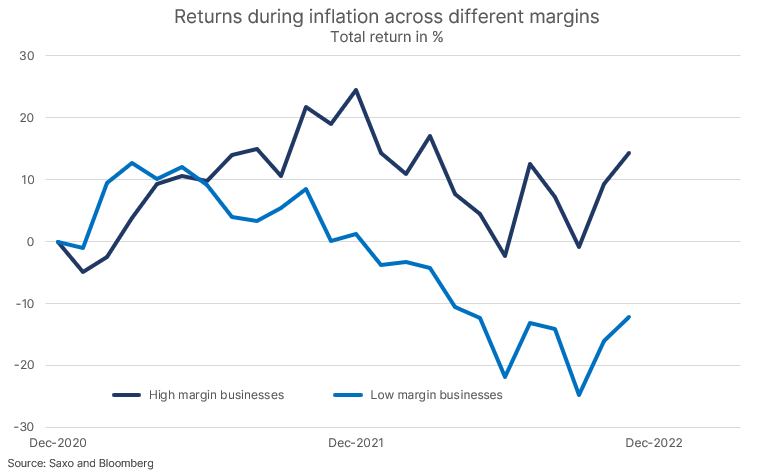

Companies with low margins become less competitive in times of inflation

When we published our thematic basket for the largest capitalization companies, one of our main arguments was that during the inflation period their performance is above average due to market power, brand recognition, wider and cheaper distribution and access to cheaper capital.

As we have described in numerous stock market analyses, inflation hits consumers and industries in very different ways, but one thing is common – the cost of capital is rising, raising the minimum acceptable rate of return for companies in terms of generating shareholder value. In the 70s a lot was aware of this phenomenon Warren Buffett and the experience of inflation prompted him and Charlie Munger to search for companies with a strong competitive advantage.

The initial wave of inflation was tolerable for most businesses, as the excess of stimulus meant that firms could easily pass on rising costs with minimal negative business impact. The second wave began late last year, culminating in the Fed's move away from its belief in the transitory nature of inflation, causing a shock to interest rates the following year.

The second phase of inflation is not as easy as the firstas workers are now demanding compensation for their lost purchasing power, significantly increasing wage pressure in the economy. For companies with low margins, this is a worrying dynamic. The fact that you have a lower margin means that you are more sensitive to wage pressure than a competitor with a higher margin, or simply companies with higher margins in the same sector.

Impact of interest rate sensitivity

The market recognized this dynamic in its valuation. The chart below shows the 10% of companies with the highest operating margins in the manufacturing sector in North America and Europe, compared to the 10% of companies with the lowest operating margins since December 2020, when inflation began to accelerate. Part of the difference in total return is repricing due to higher interest rates, as low-margin companies tended to have higher duration (interest rate sensitivity) from higher stock valuations, however, the average C / Z ratio 10% of companies with the highest margins in December 2020 was 41,5, the impact of interest rate sensitivity is therefore most likely minimal.

In the short term this may seem irritating to the boards of companies with low margins, because the profits are smaller, but the long-term impact can be much more destructive.

Due to their greater sensitivity to wage pressures, low-margin companies will not compensate their employees for inflation to the same extent as high-margin companies, which can lead to greater employee turnover, brain drain, or forcing low-margin companies into mass layoffs, which could mean a shock to the company's productivity that will hold back growth for many years. The market understands this dynamic and that is why companies are rewarded for increasing profitability, not for increasing revenue.

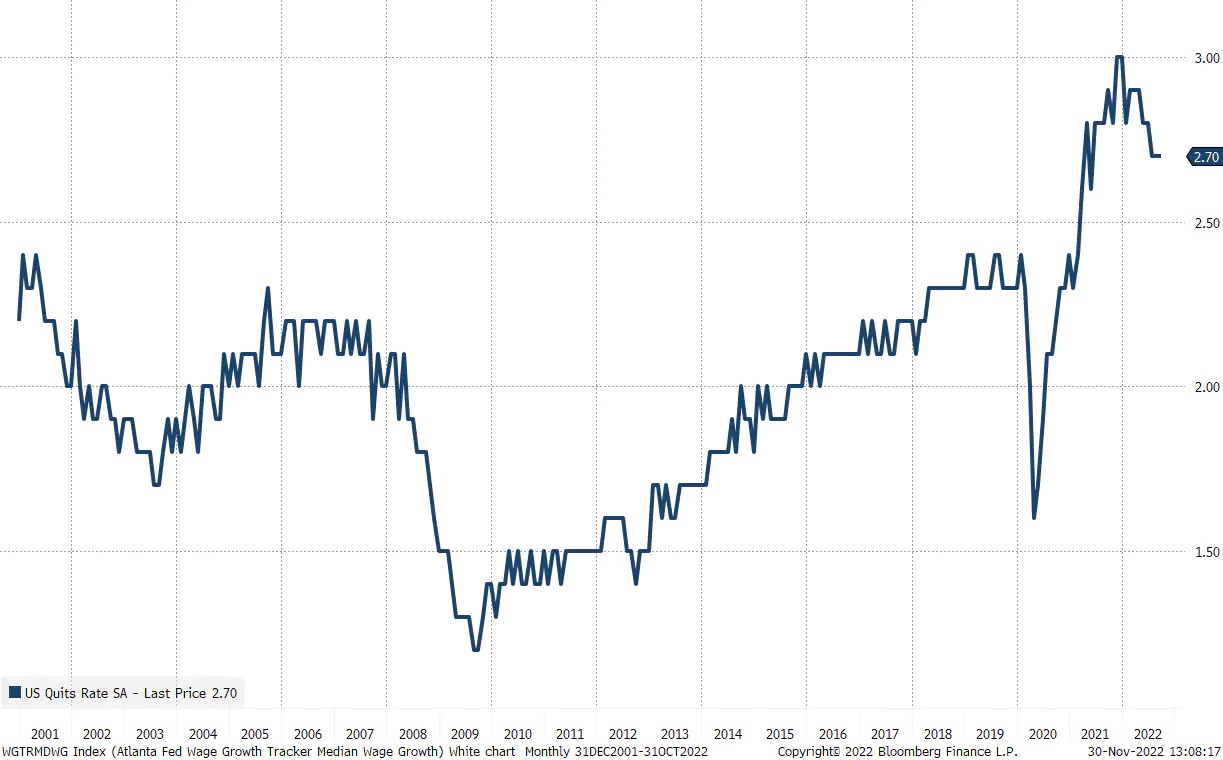

The churn rate in the United States, i.e. the number of people on the labor market who voluntarily resign from employment, is at a very high level, which suggests that the annual turnover in the American labor market is around 30%. With people leaving their jobs seeing wage increases twice the current average in the US, i.e. from around 6,5%, the pressure on businesses is now significant.

The dynamics of the wage pressure and its impact on the net profit margin is a key factor our negative view on earnings next year, as companies will find it difficult to offset the compression of margins resulting from the increase in salaries in the event of an economic slowdown.

About the Author

Peter potter - director of equity markets strategy in Saxo Bank. Develops investment strategies and analyzes of the stock market as well as individual companies, using statistical methods and models. Garnry creates Alpha Picks for Saxo Bank, a monthly magazine in which the most attractive companies in the US, Europe and Asia are selected. It also contributes to Saxo Bank's quarterly and annual forecasts "Shocking forecasts". He regularly gives comments on television, including CNBC and Bloomberg TV.